Investment fraud red flags can be easy to miss when an opportunity feels urgent, exclusive, or unusually profitable. That is exactly why buyers, investors, professionals, and families should slow down before sending money, signing documents, or sharing private financial information.

Modern investment fraud does not always look obvious. It can appear as a polished website, a friendly social media contact, a confident “advisor,” a real estate opportunity, a crypto platform, a private lending deal, a franchise pitch, or a recovery service claiming it can get lost money back.

Some schemes are aimed at experienced investors. Others target people who are buying into a business, helping a family member, or trying to build financial security.

Understanding investment fraud red flags gives you a practical filter before trust turns into exposure. This guide explains the warning signs Canadian investors should know before they commit. It is general legal information, not advice about a specific investment or case.

If the situation has already become criminal, regulatory, or urgent, Kisel Law’s fraud defence services and white collar crime pages can help you understand where these issues may fit within a broader legal matter.

Why Investment Fraud Red Flags Matter More Than Ever

Investment fraud red flags matter because fraud often begins with trust. The more ordinary the opportunity appears, the more useful these warning signs become as a decision-making checklist.

A person may trust a friend’s referral. They may trust a clean-looking website. They may trust someone who uses industry language, shows screenshots of profits, or claims to be connected to a well-known company.

They may also trust urgency because “the window is closing,” “the price is going up,” or “only a few spots are left.”

That pressure can lead people to skip basic checks.

Before investing, Canadian investors can use official tools such as the Canadian Securities Administrators’ registration search or the Ontario Securities Commission’s Check before you invest resource. These checks do not guarantee that an investment is suitable or safe, but they can help identify whether a person or firm appears registered to sell investments or give investment advice.

A common question is: “If someone is not registered, does that automatically mean it is fraud?”

Not always. Some activities may be exempt, and not every business proposal is a securities offering. But an unregistered person giving investment advice, selling securities, or pressuring you to transfer money should make you pause. It is one of the investment fraud red flags worth taking seriously.

11 Investment Fraud Red Flags to Watch For

Not every warning sign proves wrongdoing. But when several appear together, the risk increases.

Here are 11 investment fraud red flags that deserve careful attention.

| Red flag | What it may look like | Why it matters |

|---|---|---|

| Guaranteed returns | “No risk,” “fixed profit,” or “can’t lose” | Real investments carry risk |

| Urgency | “Today only” or “spots closing” | Pressure reduces due diligence |

| Secrecy | “Do not tell your bank, lawyer, or family” | Isolation helps fraud succeed |

| Unregistered sellers | No clear registration or vague licensing claims | Investors may lack protection |

| Complex payment requests | Crypto, wires, gift cards, or third-party accounts | Money may be hard to trace |

| Fake proof | Screenshots, dashboards, or testimonials | Visuals can be manipulated |

| Withdrawal problems | New fees before funds are released | A common escalation tactic |

| Romance or friendship pressure | Investment pitch tied to emotional trust | Scams can develop slowly |

| Missing documents | No clear contract, offering memo, or receipts | Rights and obligations become unclear |

| Name-dropping | Claims of celebrity, bank, or government backing | Authority can be faked |

| Recovery promises | “We can get your lost money back for a fee” | Victims may be targeted twice |

Red Flag 1: Guaranteed Returns With Little or No Risk

One of the most common investment fraud red flags is the promise of guaranteed returns.

Legitimate investments can be strong, conservative, speculative, secured, unsecured, regulated, or private. But they still involve risk. Markets change. Borrowers default. Tenants leave. Businesses fail. Crypto prices move. Real estate projects run into delays.

A promise that removes all risk should be questioned.

For example, a person may be told: “You will earn 4% every month, guaranteed, and your principal is protected.”

That sounds reassuring. But the better questions are: Who is guaranteeing it? What assets support the guarantee? Is the guarantor financially able to pay? Is the investment registered or exempt? Is there a written agreement? Is the person selling it allowed to do so?

If the answers are vague, that is not a small detail. It may be the core problem.

Red Flag 2: Pressure to Move Fast

Investment fraud red flags often appear in the timing.

Fraudsters know that time helps people think. Time allows someone to call their bank, speak with a lawyer, check registration, read documents, search the company name, or ask a trusted person for a second opinion.

So the pitch often creates urgency.

You may hear that the opportunity closes tonight. You may be told that other buyers are waiting. You may be warned that asking too many questions will cause you to lose your place.

A real opportunity should survive reasonable due diligence. If the person becomes angry, defensive, or insulting when you ask for time, step back.

This is especially important for private business purchases, real estate-linked investment offers, franchise opportunities, or cross-border deals where the documents may be more complicated. Kisel Law’s regulatory law and professional discipline page may also be relevant where investment issues overlap with securities, licensing, or tribunal proceedings.

Red Flag 3: The Seller Wants Secrecy

Another major warning sign is secrecy.

You may be told not to speak with your bank because “banks do not understand this space.” You may be told not to speak with your spouse because “they will only scare you.” You may be told not to call a lawyer because “legal review slows everything down.”

That is one of the most dangerous investment fraud red flags.

A legitimate investment professional should expect questions. They should understand that investors may want independent legal, accounting, or financial advice. They should not pressure you to hide the transaction from people whose job is to help you assess risk.

Secrecy also matters in criminal investigations. When digital messages, transfer records, contracts, or screenshots become evidence, context can be critical. Kisel Law’s guide to criminal disclosure in Ontario explains why reviewing records carefully can matter once a case enters the court process.

Red Flag 4: Unusual Payment Instructions

Payment method can reveal a lot.

Be cautious if you are asked to send funds to a personal account when the investment is supposedly corporate. Be cautious if money must be sent through cryptocurrency, multiple wire transfers, offshore accounts, prepaid cards, or third-party “escrow” services you cannot verify.

This does not mean every crypto transaction is fraudulent or every wire transfer is suspicious. But unusual payment instructions are investment fraud red flags because they can make recovery difficult and obscure who actually received the money.

A practical step is to ask for the legal name of the receiving entity, banking details in writing, invoices, receipts, and a clear explanation of why that payment route is being used. If the explanation changes, pause.

If police later search devices, seize records, or review banking messages, Kisel Law’s article on police searching phones in Canada may help explain why digital records can become important in fraud-related cases.

Red Flag 5: The Paperwork Does Not Match the Pitch

Documents should clarify a deal. They should not create more confusion.

A pitch may promise secured returns, ownership, voting rights, monthly income, or guaranteed repayment. But the paperwork may say something different. It may describe the funds as a loan, a subscription, a donation, a service fee, a membership, or a “private opportunity” with no clear rights at all.

That mismatch is one of the investment fraud red flags buyers and investors should not ignore. For buyers reviewing a business, property-linked deal, or private placement, investment fraud red flags often appear first in the paperwork.

Read the documents slowly. Look for names, dates, repayment terms, risk language, fees, dispute clauses, signatures, governing law, and whether the person selling the investment is actually a party to the agreement.

If the contract is missing basic details, that is not just poor drafting. It may make it harder to understand what you are buying.

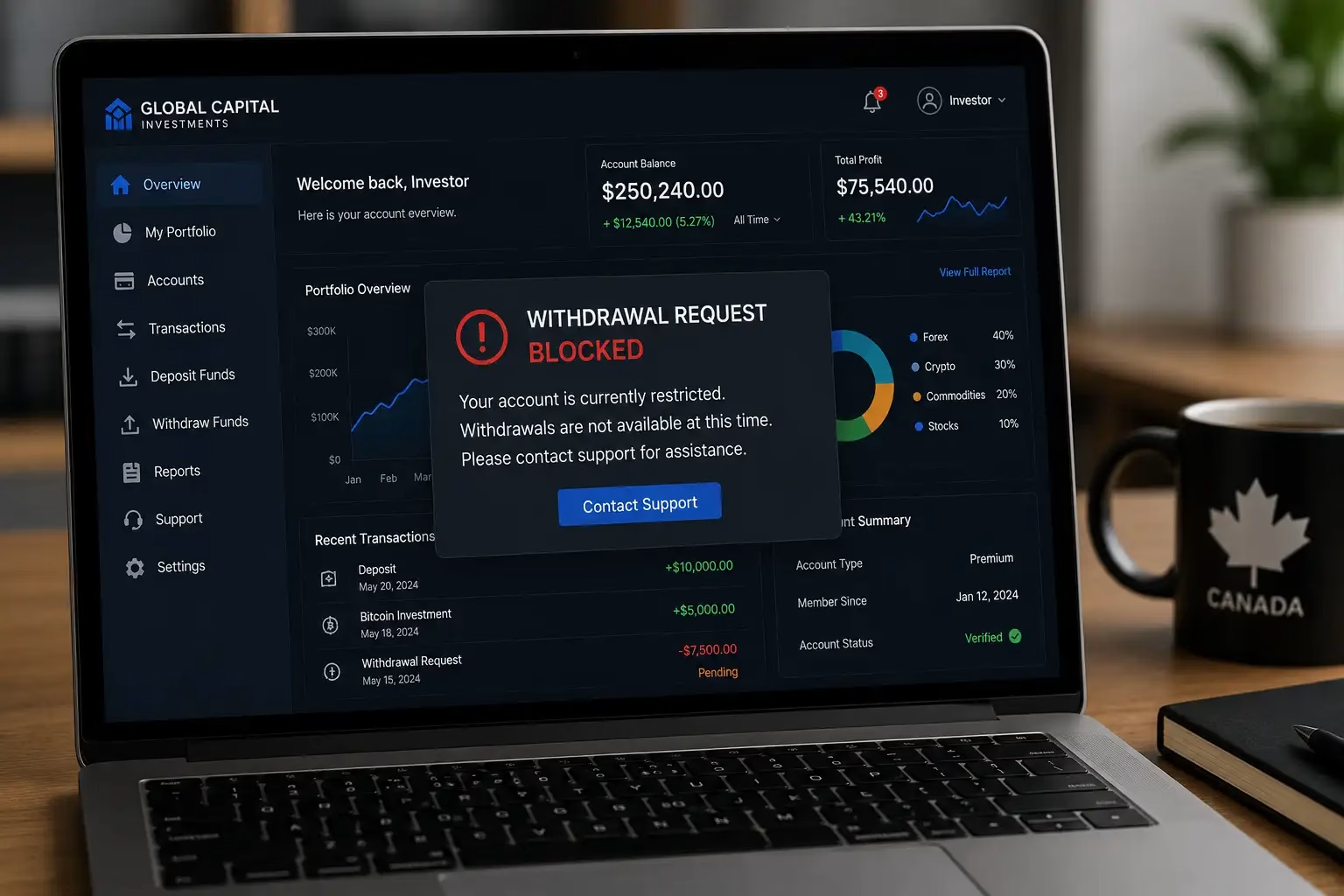

Red Flag 6: Online Dashboards Show Profits You Cannot Withdraw

Many modern scams use dashboards.

The investor logs in and sees profits rising. The numbers look impressive. The platform may show charts, deposits, bonuses, referral rewards, and projected returns. Then, when the investor tries to withdraw money, problems appear.

There may be a tax fee, release fee, verification fee, anti-money-laundering fee, wallet fee, or upgrade fee. Each payment is framed as the last step before funds are released.

Withdrawal problems are among the clearest investment fraud red flags. A dashboard is not proof that money exists. It is only a screen showing information someone controls.

If this happens, avoid sending more funds until you have independent advice. You can also review general fraud reporting information from the Canadian Anti-Fraud Centre and consider contacting your bank or financial institution quickly.

Red Flag 7: The Opportunity Arrives Through Romance, Friendship, or Social Media

Some scams begin as relationships.

A person may connect through social media, a dating app, a business group, WhatsApp, Telegram, Instagram, LinkedIn, or a community chat. The conversation may feel personal before it becomes financial.

The person may not ask for money immediately. Instead, they build trust, show lifestyle photos, mention investing casually, and later introduce a platform.

This slow approach can make investment fraud red flags harder to recognize because the pitch does not feel like a pitch.

A useful test is simple: Would you trust this opportunity if it came from a stranger in a cold email?

If the answer is no, the relationship should not replace due diligence.

Red Flag 8: The Seller Uses Credentials You Cannot Verify

Fraudsters often borrow credibility.

They may claim to be registered advisors, former bankers, accountants, lawyers, real estate experts, crypto analysts, government-connected consultants, or representatives of a known firm. They may use logos, email signatures, copied biographies, fake certificates, or names that look similar to legitimate companies.

Do not rely only on what they send you.

Check registration independently. Search official sources. Call the organization using a number from its official website, not a number provided in the pitch. Review investor alerts from regulators such as the Ontario Securities Commission investor warnings and alerts if the name feels unfamiliar.

False credentials are investment fraud red flags because they are designed to make you stop asking questions.

Red Flag 9: The Explanation Is Too Complicated to Challenge

Some investment pitches sound sophisticated because they are hard to understand.

The person may use terms like liquidity pools, arbitrage, private placement, bridge financing, offshore insurance wrap, tax shelter, AI trading, mining allocation, guaranteed token yield, collateralized note, or institutional block trade.

Some of those terms can exist in legitimate contexts. But jargon can also be used to hide risk.

A good explanation should become clearer when you ask questions. If it becomes more confusing, that is a problem.

Ask: What am I buying? Who holds the money? How is profit created? What could go wrong? How do I exit? What fees apply? What documents prove ownership? Who regulates the seller?

If the seller cannot answer plainly, treat that as one of the investment fraud red flags.

Red Flag 10: You Are Told to Mislead the Bank

A serious warning sign appears when someone coaches you on what to tell your bank.

They may say: “Do not say it is for crypto.” “Tell them it is for renovations.” “Say it is for a family loan.” “Do not mention the platform.” “Break the transfers into smaller amounts.”

That is extremely risky.

Banks may ask questions because fraud patterns are common. Lying to a bank can create further complications, especially if the transaction later becomes part of a criminal, regulatory, or civil dispute.

If someone asks you to mislead a financial institution, you are not just seeing investment fraud red flags. You may be facing a situation that needs immediate independent advice.

Red Flag 11: A Recovery Service Contacts You After a Loss

Unfortunately, victims can be targeted again.

After someone loses money, another person may appear claiming they can recover it. They may say they work with regulators, police, blockchain experts, banks, courts, or foreign agencies.

They may promise fast recovery in exchange for an upfront fee.

Recovery pitches can be emotionally powerful because the person is already stressed and wants hope.

Be careful. Real recovery can be difficult, slow, and uncertain. Anyone promising guaranteed recovery for a fee should be treated cautiously. Keep records, avoid sending more money, and consider reporting the contact.

What Should You Do If You Notice Investment Fraud Red Flags?

If you notice investment fraud red flags before sending money, slow everything down. Treat these warning signs as a reason to verify, not as a reason to panic.

Do not let embarrassment, urgency, or fear push you into a decision.

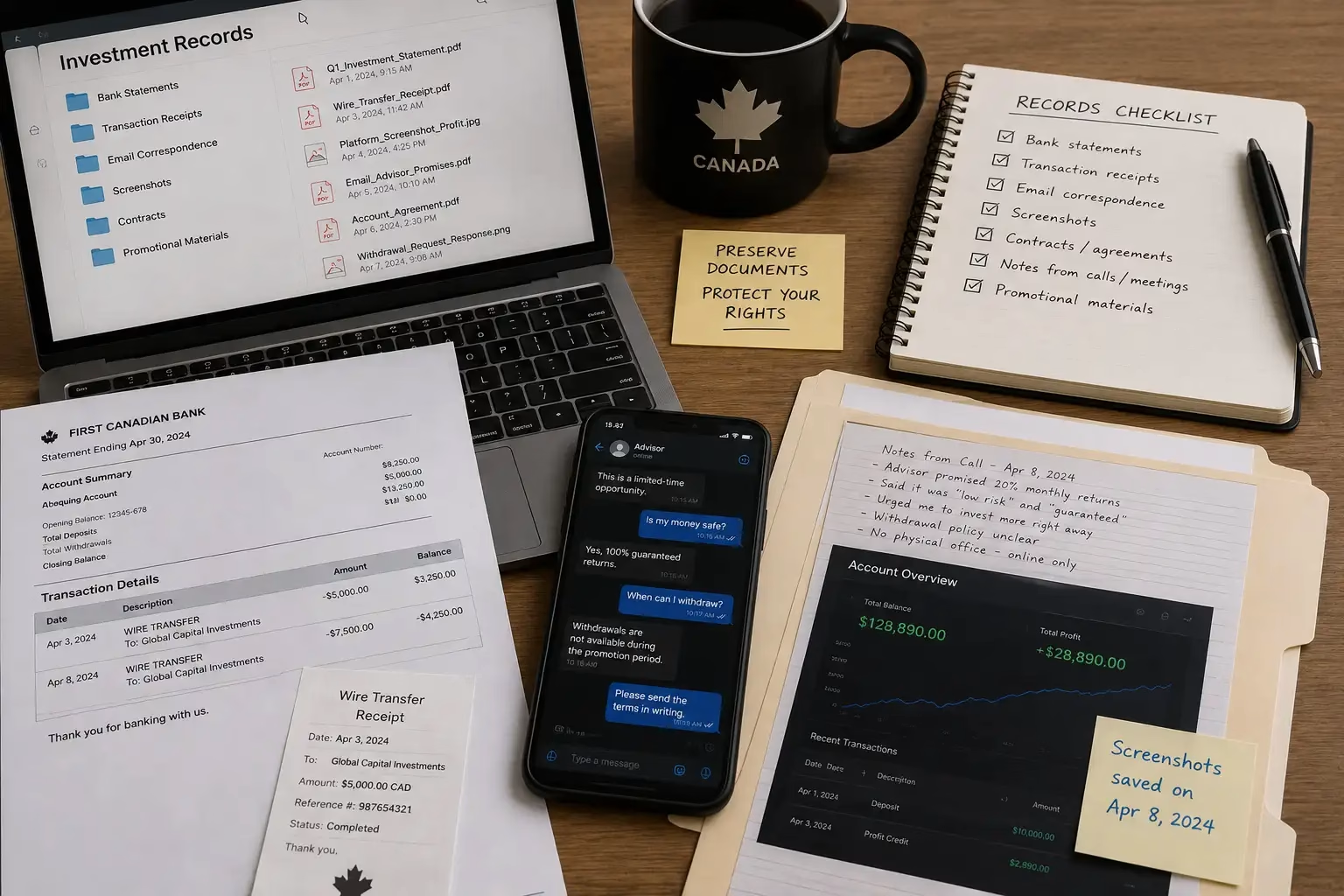

Save messages. Screenshot the website. Keep emails, contracts, receipts, wallet addresses, names, phone numbers, and banking details. Search the company and person independently. Check registration. Speak to someone who is not emotionally involved in the deal.

If you already sent money, the steps may be different:

- Contact your bank or financial institution quickly.

- Stop sending additional funds.

- Preserve every record.

- Report suspected fraud through appropriate channels.

- Avoid confronting the person in a way that causes evidence to disappear.

- Get legal advice if you are accused, contacted by police, under investigation, or unsure about your exposure.

If charges, bail, release conditions, or court dates are already involved, Kisel Law’s resources on bail hearings, an undertaking in Ontario, and a judicial pre-trial in Ontario may help you understand the next procedural steps.

How Investment Fraud Can Become a Criminal or Regulatory Issue

Investment fraud red flags do not only matter to victims.

They can also matter to people accused of fraud, business partners, advisors, employees, professionals, directors, or family members whose names appear on documents or accounts.

In some cases, a person may believe they were helping with a legitimate business. In others, someone may be accused of misleading investors, handling funds improperly, using false statements, or participating in a broader scheme.

Fraud-related cases can involve bank records, phone data, contracts, emails, investor communications, corporate records, regulatory notices, search warrants, and witness statements.

They may also overlap with fraud and theft allegations, insurance fraud, professional discipline, or white-collar investigations.

This is why early legal guidance matters. The facts, documents, timing, and communications can change how the situation is understood.

Final Thoughts: When Investment Fraud Red Flags Become Legal Concerns

Investment fraud red flags are not about being suspicious of every opportunity. They are practical warning signs that help you separate confidence from proof.

A careful investor asks questions. A careful buyer verifies documents. A careful professional protects records. A careful family member does not let urgency replace judgment.

If you are reviewing a questionable investment, dealing with a loss, facing allegations, contacted by police, or concerned that your name appears in a fraud-related matter, Kisel Law can help you understand the legal side of the situation.

Kisel Law represents clients in Toronto and surrounding communities, including those seeking a criminal lawyer in Toronto, Mississauga, Brampton, Vaughan, Richmond Hill, Ajax, or Pickering.

To learn more about the firm, visit Nicole Kiselyov’s profile, explore Kisel Law’s criminal defence practice areas, or contact Kisel Law to discuss the next step.